by Nicki Hutley, COBA’s Chief Economic Adviser

Australia’s house prices, housing affordability, the housing and rental crisis – every day there are new stories in media about the nation’s property sector. But how did we get here? Economist Nicki Hutley gives insight into what’s causing prolonged high prices in the property market, and what it might mean for you.

These days, the problem of housing affordability – for both owners and renters – never seems to be far from the headlines.

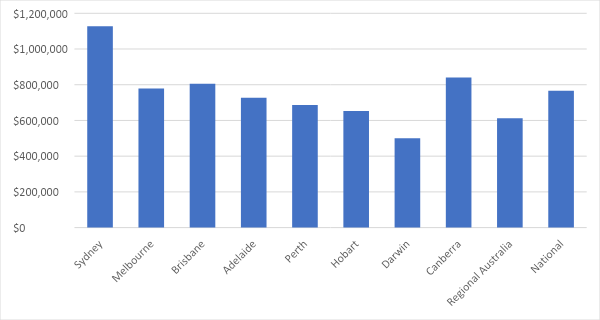

We are now back to record house price levels in most parts of Australia, including regional areas. In Sydney, that means the median price of a dwelling is now $1.1 million, almost half as much again as the median dwelling in Melbourne and 40% higher than in Brisbane. Canberra now is the second-most expensive city for housing.

Median dwelling prices ($) March 2024

We have had thirteen interest rate rises over the past two years. Usually, this puts a big dampener on housing prices. When rates first started rising, house prices did soften for a little while in most areas of Australia, but that did not last for long.

There are a few reasons for this:

- Our population has increased very rapidly over the past couple of years. This followed a long time when our borders were closed, so much of this is catch up and ensuring we have enough workers and that international students can take up studies again.

- We haven’t built enough houses. Not only do we have more people to build for, but many of us are choosing to live in smaller household sizes. Part of that trend is because we’re having smaller families and people living longer and staying in their homes. Our planning systems have let us down, by not allowing more homes in areas where they are need, close to train lines, schools, shops, and hospitals.

- Even though interest rates have risen, they are still pretty low compared to much of recent the past. And with government incentives for investors like negative gearing, we have more people competing for the one home.

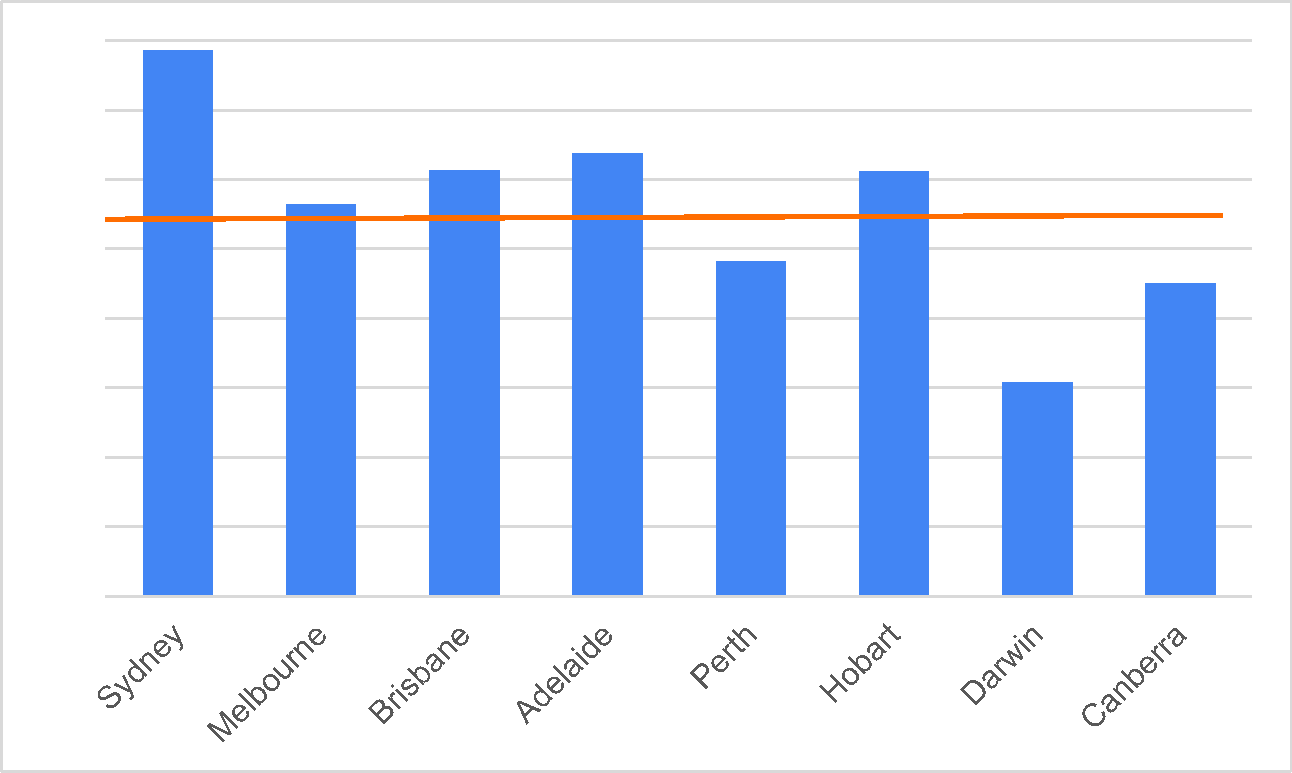

With house prices so high, younger Australians are particularly impacted. If you don’t have parents or grandparents able to help you with a deposit, it will take on average nearly 11 years for someone to save enough for a deposit. If you’re just starting out on a very low salary, that could double. And if you live in Sydney, even on an average wage, it’ll take you nearly sixteen years of very hard saving.

Years to save for a deposit

And even if you can save for a deposit, someone buying a house today will have to pay well over 30% of their income to service their mortgage, unless they buy in Darwin.

If you’re a homeowner, higher house prices are good. They add to your wealth and make you feel more confident. But if you’re trying to get into the market, it is now very challenging. Policies aimed at helping younger Australians into home ownership, or providing good options for rental accommodation, need to be fair. Above all, they need to be focused on increasing the supply available. Otherwise, our kids may be living with us until they are 50 instead of 30!